It was January 10, 1995 — the day after my 10th birthday. Throughout the week I received my favorite gift from friends and family. That favorite gift was money. I would love to say with 100% confidence that these monetary gifts accompanied heart-filled cards, but I honestly don’t remember because I opened the cards anticipating a mild thunderstorm. Anyway, after memorizing the exact amount that I had accumulated, my mother suggested that I open a savings account rather than constantly ask her where my money was. So on this 1995 winter day, we headed to the bank to open a junior checking account. The experience was typical of the times and as a child I simply accepted it. I walked into a branch, that I swear was an abandoned McDonald’s two years prior, and my mother spoke to a personal banker that I gave my birthday money to. In return, I got a printout stating how much money I gave the personal banker. As a 10-year-old I thought it was either magic or an inefficient system.

Nothing Was The Same..I mean Different

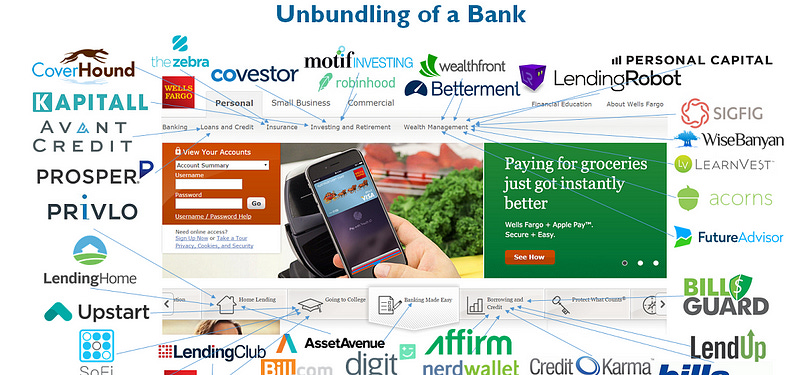

Twenty years later, despite advances in technology, the process of opening accounts looks very similar. It makes no sense that large banks have not innovated given macroeconomic issues and changes in customer preferences. The economic downturn caused numerous banks to eliminate substantial stakes in non-lucrative lines of business such as student lending, small business loans, and free checking accounts. These decisions have resulted over the past 8 years with the emergence of alternative lending startups such as LendingClub, OnDeck, SoFi and Earnest (I love that name for some reason) that have contributed to what many FinTech experts call the “unbundling of the traditional bank.” The gap left by banks has been filled by these tech-enabled businesses. However, why have banks or FinTech firms not focused on providing banking to a majority of our domestic population — also known as the under-banked? There is an opportunity (and I mean potential for profit and not just mission oriented) in this market due to potential volume and the cost-saving opportunities of mobile banking.

Traditional Banks Can’t Afford to Serve this Market

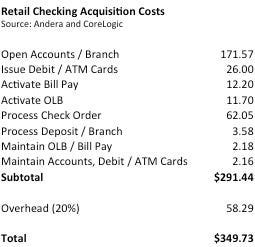

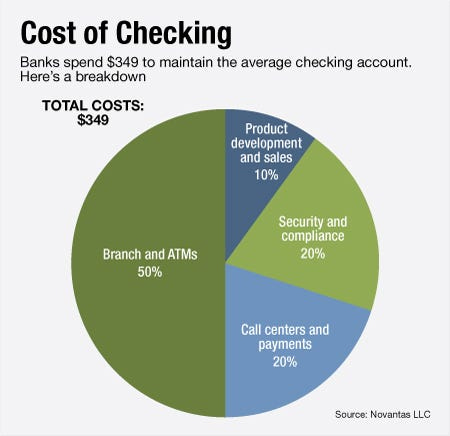

Traditional banks have typically not focused on serving the under-banked through financial inclusion efforts because of their prolonged use of the same archaic processes and expense structures that I first experienced in 1995. The cost metrics of banks vary depending on factors such as size, channel management, and technology & staffing efficiency. However, several studies have indicated that customer acquisition expenses range between $300-$400 per retail checking customer. The figures below from the Andera/CoreLogic and Novantas studies break down the contributing costs that make up the ~$350 total acquisition cost. To no surprise branches account for a majority of these expenses.

The revenue trends associated with checking accounts shed more light on why banks have stayed away from offering free checking or other customer friendly products to the under-banked. The average revenue per account is just $268, which suggests a loss of $81 when incorporating the $350 acquisition cost estimate. Despite a large number of potential customers within the under-banked market in the United States, banks just can’t afford to play in this market. This is similar to why banks have decreased lending to small businesses. It’s simple math: when cost > revenue when underwriting a loan or, in this case, providing a no flat fee product — no matter how large the total market, your business will continue to lose money (Yay, I got an MBA to let you all know that profit less than zero is bad). It is also important to remember that the average revenue figure is more than likely much higher than accounts that are lower in deposits. To recoup costs of serving customers who keep small deposits, banks have increased fees. This generally has impacted the under-banked. According to the FDIC, nearly 70 million Americans are currently under-banked by traditional financial services, making managing money difficult and expensive for a large segment of the U.S. population who are living largely in a cash economy in an increasingly digital environment.

Trends Provide Great Conditions for Mobile-Only Banks

From a macro perspective, I believe technology is providing new options for the millions of Americans who are currently under-banked by traditional banks and credit unions. Mobile phones are becoming the gateway to the economy for under-banked consumers. Customers are more accustomed to conducting transactions over their mobile devices. This shift in consumer mindset should enhance digital literacy and increase digital inclusion. Also, a larger proportion of under-banked consumers in the U.S. own mobile phones and smartphones — and use mobile financial services — relative to the total U.S. population. This why Hank Israel, of Novantas LLC, believes “[fintech startups] are really in a position to acquire these customers. They have lower cost structures because they either organize themselves online or have very concentrated focuses.” Another study done by consulting firm Javelin Strategy & Research found that mobile banking decreases cost per transaction by 98%. The study also stated the following insights:

* In-person transaction at a physical branch cost a bank $4.25, while a phone call to a call center or the use of an ATM cost $1.29 or $1.25, respectively

* Mobile banking transactions cost just 10 cents, and online banking transactions cost just 19 cents

* Customers not using online banking cost banks $359 a year. That was $167 more than the annual cost of $192 for customers using online banking services

Disruptive BEEcause of the Target Market

As I’ve been getting more and more immersed in the fintech ecosystem, I have come across a common argument against investing in sub-sectors such as mobile banking and alternative lending. This debate is centered around the question: “Is it truly disruptive?” Some believe that most of these new startups are simply completing the same processes at a faster rate through technology. The “not-disruptive” camp contends that if a company does not have potential to kill off the large market leaders (banks) then they can’t characterize themselves as disruptive. I understand that mobile banking has been around for about 15 years, but I don’t feel mobile-only banks targeting the under-banked lacks innovation. Successfully establishing a company that serves those that have been characterized as a net-negative sets the stage for disruption.

One company that is testing this thinking and developing the product market fit for a mobile-only bank is BEE, the first product provided by One Financial Holdings. I met the CTO & co-founder, Max Gasner, a year ago and have kept in touch with the progress of the firm. Earlier this year they launched their product in Brooklyn and within the first three months were servicing thousands of customers and employed a number of highly competent/personable tellers. Companies like BEE are in a strong position to prove the profitability of a large scale mobile-only bank. The potential of providing the under-banked a breadth of products/services while eliminating predatory fees is the definition of disruption to me.

#IWBITK (I Would Be Interested to Know) What’s your thoughts on mobile banking for the under-banked? Do you think it is disruptive or not?