Who Puts You in Business

Why the next generation of venture firms will be incubated, not raised

A few months ago, I kept hearing the same question in different accents.

From LPs, sometimes on the record, sometimes off.

From GPs, especially the ones with real scar tissue and a real point of view.

From operators circling the industry, wondering if the door is closing.

The question is simple:

If more capital is being gobbled up by the biggest brands in venture and growth capital, how will new firms ever break through?

It is a fair question. It is also the wrong mental model.

Because if you look at how the great franchises in venture were actually born, you start to see a pattern.

Most enduring firms did not simply “raise a fund.”

They were put in business.

Some LP, or small group of LPs or individuals, stuck their neck out. They wrote the first meaningful check. They recruited the next check. They gave the GP the oxygen to build. Not just invest.

And in this market, where attention is scarce, and patience feels like an endangered species, I think we are about to see that formation mechanism evolve.

Not disappear.

Evolve.

The chasm is real, but it is not new

Venture always had a power law. It always had brand gravity. It always had inside lanes.

What feels different now is the shape of the market.

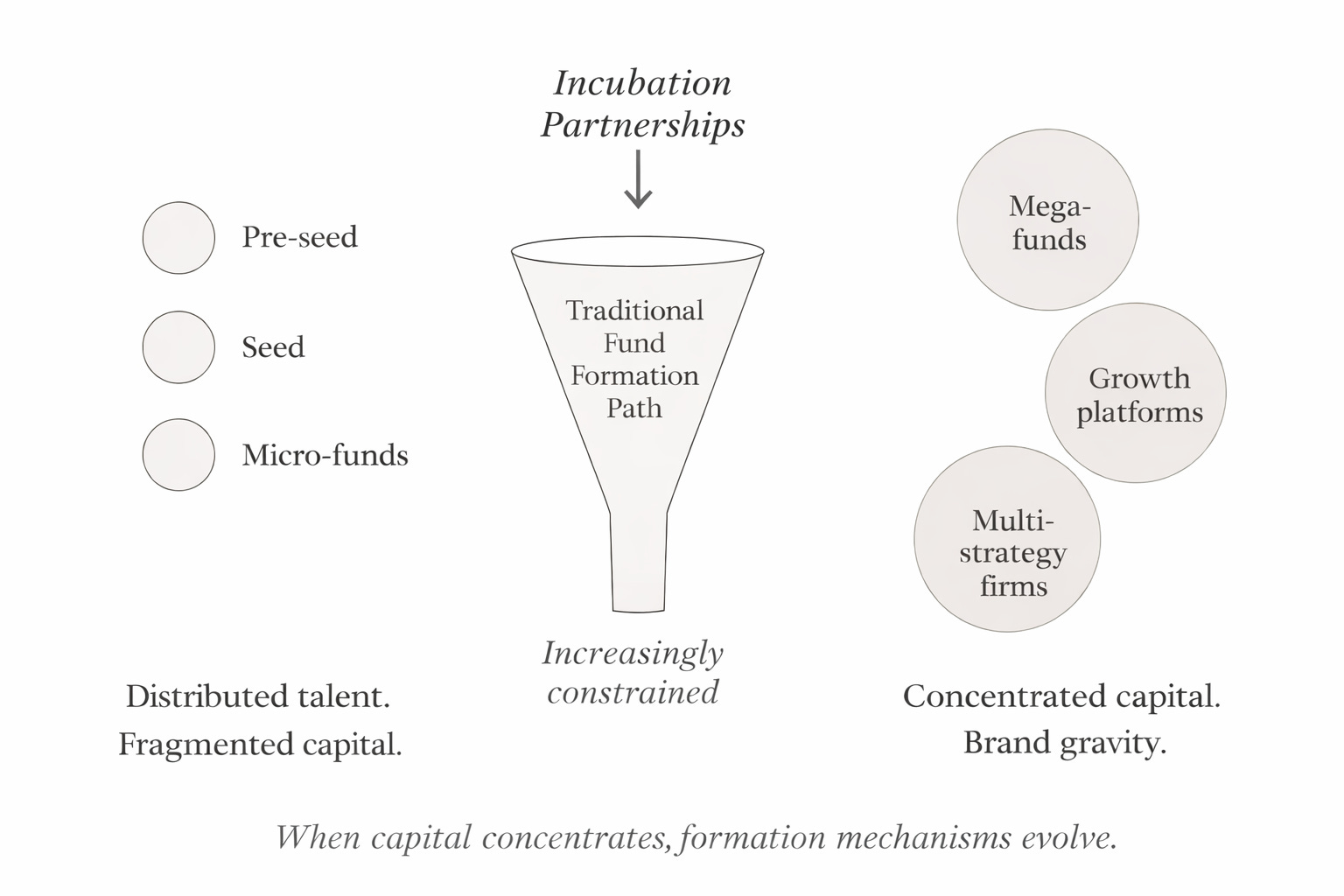

Upstream, you have an explosion of managers at pre-seed and seed. Some are excellent. Many are loud. The ecosystem is more distributed than ever.

Downstream, you have mega-funds and growth platforms consolidating capital, talent, and mindshare. More dollars. More infrastructure. More ways to win deals.

And in the middle, you have the zone where franchises used to get built.

The Series A and Series B layer that could grow into a fund-to-firm-to-franchise over time.

That middle layer is not dead, but the on-ramp is harder.

Not because there are fewer great investors.

Because the old formation path is getting squeezed by two forces at once:

Capital concentration

Trust compression

Capital concentration is obvious. Bigger funds have more capital and more momentum.

Trust compression is subtler. Everyone is trying to decide faster. Committees want fewer unknowns. Founders want fewer meetings. LPs want fewer surprises in a market that has plenty.

When those two forces hit at the same time, “raising your first fund” becomes less like a rite of passage and more like an obstacle course.

The numbers explain why this feels different.

By 2024–2025, the top tier of venture firms captured a disproportionate share of new capital. Depending on the dataset, roughly the top 10–15 firms by fund size raised between 35–45% of all venture dollars in a given vintage, while the top 25 firms captured well over half.

At the same time, the number of active venture funds continued to grow, and median fund sizes either flattened or declined. In other words, more managers were competing for a smaller slice of discretionary capital, while brand-name platforms absorbed the majority of commitments.

This is not just capital concentration. It is formation pressure. The market is signaling that scale, trust, and distribution matter earlier than they used to.